Stocks sag ahead of monthly jobs report

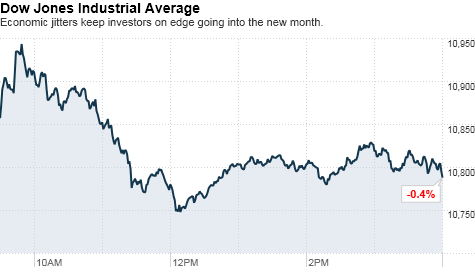

NEW YORK (CNNMoney.com) -- Stocks finished mixed after a sluggish session Thursday afternoon, as cautious investors paused and geared up for the monthly jobs report due Friday.

The Dow Jones industrial average (INDU) closed down 19 points, or 0.2%. The blue chip index started off the day with a pop and was less than 2 points shy of the 11,000 mark, a level it hasn't traded at since May. But the Dow drifted as the session wore on and sank almost 75 points before recovering.

The S&P 500 (SPX) lost 2 points, or 0.2%, while the tech-heavy Nasdaq (COMP) added 3 points, or 0.1%.

Stocks surged earlier this week, with all three major indexes hitting 5-month highs. But investors have had trouble keeping up that momentum, as reports showed continued weakness in the labor market.

Some of that sentiment briefly lifted Thursday morning as weekly jobless claims fell to a 3-month low, but traders remain wary ahead of the the true test -- Friday's monthly payrolls report.

"We're likely to have a muted day on Wall Street because the of September jobs report coming up tomorrow," said Timothy Ghriskey, chief investment officer at Solaris Asset Management. "We still have incredible weakness in the job market, so there is some concern leading up to the numbers."

According to a consensus of economists polled by Briefing.com, the number of jobs is expected to remain flat in the upcoming monthly report. At the same time, the unemployment rate is expected to have ticked up to 9.7% from 9.6%.

Ghriskey added that investors will also be cautious as companies begin reporting third-quarter financial results.

While PepsiCo (PEP, Fortune 500) reported results in line with forecasts before the bell Thursday, Ghriskey said the company's performance is not as reflective of broader economic conditions as a company like aluminum maker Alcoa (AA, Fortune 500). Alcoa, which delivered results after the market close Thursday, will also be in focus during Friday's trading session.

Stocks also felt some pressure Thursday afternoon as the dollar gained ground. Though it remained broadly weaker, the buck clawed back and rallied against the euro, which had climbed above $1.40 earlier Thursday. It also moved higher versus the pound.

The dollar index, which measures the greenback against a basket of rival currencies, gained almost 0.4% before easing back.

Economy: The initial jobless claims number was the lowest in nearly 3 months, providing a breath of fresh air to the market. The Labor Department on Thursday reported that jobless claims totaled 445,000 in the week ended Oct. 2 -- down 11,000 from the prior week.

Economists were expecting the government to report 455,000 Americans filed for unemployment for the first time last week, pointing to continued weakness in the job market.

Investors are also eyeing retailers' September same-store sales figures Thursday for indications about consumer spending. Thomson Reuters, which tracks same-store sales for a group of 28 national chains, said total sales for the group rose 2.8% in September -- better than its initial forecast of a 2.1% gain in the month.

Companies: Rumors that Apple (AAPL, Fortune 500) is preparing a version of its iPhone for Verizon (VZ, Fortune 500) -- the phone is currently only carried by AT&T (T, Fortune 500) -- started swirling again, after the Wall Street Journal published a report saying the phone may be on shelves early next year. Apple's stock edged higher as Verizon's slipped.

PepsiCo (PEP, Fortune 500) was the first major company to report third-quarter results Thursday. Pepsi earned $1.22 per share during the quarter, in line with analysts' forecasts and up 13% from the year-ago quarter. But the beverage giant reduced the higher end of its profit outlook for the the year. Pepsi decreased about 3%.

Alcoa (AA, Fortune 500) was the first Dow component to report results. The aluminum giant raked in $61 million, or 6 cents per share. Excluding certain items, Aloca brought in 9 cents per share, topping forecasts for earnings of 5 cents per share. Sales rose 15% to $5.3 billion, beating expectations for $4.96 billion in revenue.

Adobe (ADBE) shares jumped almost 12% late Thursday after a New York Times blog reported a Microsoft (MSFT, Fortune 500) team, including chief executive Steve Ballmer, held a secret meeting with Adobe CEO Shantanu Narayen on a number of topics including the possibility of a merger between the two tech giants.

World markets: European shares finished mixed. Britain's FTSE 100 fell 0.3%, while the DAX in Germany and France's CAC 40 closed with slight gains.

Asian markets were also flat. Japan's Nikkei index and the Hang Seng in Hong Kong both finished little changed. The Shanghai Composite is closed for a week-long holiday.

Currencies and commodities: As investors anticipate another round of asset purchases from the Federal Reserve, the dollar has continued to fall against the Japanese yen.

But the greenback climbed higher against the euro and the pound after suffering sharp declines Thursday.

As the dollar gained ground, commodity prices fell under pressure.

Gold futures for December retreated from record territory. The precious metal's price fell $12.70 to settle at $1,335.00 an ounce. It had touched a new intraday high of $1,366 an ounce earlier.

The price of crude oil for November delivery decreased $1.56 cents to settle at $81.67 per barrel.

Bonds: Despite the bid for safer investments, Treasury prices were flat. The yield for the benchmark 10-year U.S. Treasury held steady at 2.40%.

Dow hits 5-month high, Nasdaq sinks

NEW YORK (CNNMoney.com) -- Stocks ended Wednesday's choppy session mixed, as cautious investors mulled two reports showing continued weakness in the job market. The news comes ahead of the closely-watched monthly jobs report due Friday.

The Dow Jones industrial average (INDU) added 23 points, or 0.2%, with GE (GE, Fortune 500) and Alcoa (AA, Fortune 500) leading the advance. The modest gains allowed the blue chip index to close at a fresh five-month high. The index's laggards included AT&T (T, Fortune 500) and Bank of America (BAC, Fortune 500).

The S&P 500 (SPX) seesawed between gains and losses, but ended the session flat, down less than one point from the five-month high it closed at Tuesday.

The Nasdaq (COMP) slumped throughout the day, and ended the session 19 points lower, or 0.8%. The tech-heavy index was dragged down as telecommunications company Equinix (EQIX) plunged 33% and computer software firm Citrix Systems (CTXS) sank 14.3%.

All three major indexes rallied 2% Tuesday to the highest levels since May. A report showing that service sector activity improved in September, and a surprise move by Japan's central bank to cut interest rates, sparked a broad-based rally.

But the enthusiasm evaporated Wednesday, as the dour jobs numbers weighed on investor sentiment ahead of the government's September jobs report on tap for Friday.

"The market remains focused on economic news, and most of the concerns are over the employment picture. So anything like today's payroll numbers reminds investors that the economy is still far from perfect, which leads to some weakness," said Matt King, chief investment officer at Bell Investment Advisors.

According to a consensus of economists polled by Briefing.com, the number of jobs is expected to remain flat in the upcoming monthly report. At the same time, the unemployment rate is expected to have ticked up to 9.7% from 9.6%.

But King said corporate earnings season, which unofficially kicks off after the closing bell on Thursday when Alcoa (AA, Fortune 500) reports its results, could lift the markets.

"We're expecting company results to show the same type of improvement we've seen for most of this year, and regain the market's attention," King said. "As those come in, stocks should move higher throughout the fourth quarter."

Economy: Payroll processing firm ADP reported the private sector jobs plunged in September, trouncing the forecast of an increase.

The U.S. economy lost 39,000 private sector jobs last month, said ADP on Wednesday -- which was much worse than expected. Economists were forecasting the report to show private sector employers added 18,000 jobs in September.

The number of job cuts planned by employers edged up slightly in September. However, the number remained near a rock bottom 10-year low reported in August, according to a report from outplacement firm Challenger, Gray & Christmas.

Employers said they would cut 37,151 jobs in September, up 7% from the 34,768 job cuts reported in August.

As traders look ahead to the government's jobs report due on Friday, they will use the ADP and Challenger reports as a gauge of the national unemployment picture.

Meanwhile, the International Monetary Fund said a double dip recession is unlikely, but global economic growth will slow from 4.8% this year to 4.2% in 2011.

Companies: Johnson & Johnson (JNJ, Fortune 500) announced a deal to aquire Dutch biotechnology company Crucell (CRXL) for about $2.43 billion. J&J already owns 17.9% of Crucell's outstanding shares and last year, the two companies started working together on a flu vaccine. Both companies' stocks finished higher.

Costco (COST, Fortune 500) said its fourth-quarter income rose 16% to $432 million, or 97 cents per share -- beating analysts' estimates of 95 cents per share. The wholesaler's earnings got a boost from increased membership sales and strength overseas. Shares rallied 1.2%.

In a continued effort to expand its $40 billion energy business, GE (GE, Fortune 500) said it is buying energy technology and service provider Dressing Inc. for $3 billion. GE's stock rose 2.4%.

Shares of AMR (AMR, Fortune 500), the parent company of American Airlines, rose 1.6% after the airline said it is bringing back hundreds of furloughed pilots and attendants, after forming joint businesses with several other airlines.

Verizon's (VZ, Fortune 500) stock climbed out of negative territory and spiked 0.9% after rumors that Apple (AAPL, Fortune 500) is building a "Verizon-ready" iPhone resurfaced in a story in the Wall Street Journal.

World markets: European shares closed with solid gains. Britain's FTSE 100 climbed 0.8%, while France's CAC 40 and the DAX in Germany advanced 0.9%.

Asian shares finished sharply higher. Japan's Nikkei index leapt 1.8% and the Hang Seng in Hong Kong jumped nearly 1.1%. The Shanghai Composite is closed for a week-long holiday.

Currencies and commodities: The dollar slipped against the euro, the British pound and the Japanese yen.

Gold futures for December delivery rose $7.40 to settle at an all-time high of $1,347.70 an ounce, after reaching a fresh intraday record trading high of $1,351 an ounce earlier.

The price of crude oil for November delivery added 41 cents to settle at $83.23 a barrel.

Bonds: Prices for U.S. Treasurys rose, pushing the yield on the 10-year note down to 2.40% from 2.48% late Tuesday. Bond prices and yields move in opposite directions.

Stocks surge to 5-month highs on Japan, services

NEW YORK (CNNMoney.com) -- U.S. stocks rallied right out of the gate and continued to surge Tuesday, with all three major indexes gaining about 2% and finishing at their highest levels since May. Investors welcomed a surprise move by the Bank of Japan to cut its key lending rate, as well as improved data for the U.S. service sector.

The Dow Jones industrial average (INDU) jumped 193 points, or 1.8%, to finish at 10,945, its highest level since May 3. Gains were broad-based as 29 of 30 Dow issues closing higher, with Boeing (BA, Fortune 500), Bank of America (BAC, Fortune 500) and DuPont (DD, Fortune 500) logging the biggest increases.

The S&P 500 (SPX) added 24 points, or 2.1%, with Harley-Davidson (HOG, Fortune 500) closing up 9.1%. The tech-heavy Nasdaq (COMP) climbed 55 points, or 2.4%. Both indexes closed at their highest levels since May 12.

Early Tuesday, Japan's central bank announced a move to lower its key interest rate to between 0% and 0.1%. It previously stood at 0.1%. The bank also said it would purchase about $60 billion of government bonds and other assets, to boost the pace of the country's recovery.

The Bank of Japan downgraded its economic forecast, but investors took the monetary policy move as a hopeful sign for the world's third-largest economy.

Investors were also encouraged after the Institute for Supply Management's index measuring U.S. service sector activity rose more than economists had forecast.

"The markets are feeling reassured after Japan's move to ease monetary policy and the fact that the service sector, which accounts for 90% of our economic activity, is stronger than we were expecting," said Jack Ablin, chief investment officer at Harris Private Bank.

U.S. stocks are coming off of a big dip on Monday, when investors were feeling cautious ahead of corporate earnings season and key employment data due later in the week. Last week, they kicked off the start of October and the fourth quarter with modest gains.

Experts said stocks will likely continue treading water, lacking day-to-day consistency, until the upcoming reports give the market a better direction.

"The lynchpin economically is still unemployment," said Erick Maronak, senior portfolio manager at Victory Capital Management. "That's what gets people off the ledge. Some improvement there would be more than welcome by investors and non-investors alike."

Economists polled by Briefing.com expect the unemployment rate to have risen to 9.7% in September, up from 9.6% in August, when the government reports the figure Friday.

World markets: Japan's Nikkei rallied 1.5% after the Bank of Japan's decision, and the Hang Seng in Hong Kong ended the session up 0.1%. The Shanghai Composite was closed for the week-long Golden Week holiday.

European stocks also finished higher. The CAC 40 in France climbed 2.3%, while Britain's FTSE 100 rose 1.5% and Germany's DAX advanced 1.3%.

European investors welcomed better-than-expected data on the euro-zone services sector, but gains were limited by fears about Ireland's debt crisis. Moody's said Tuesday that it was considering a possible downgrade for the country.

Economy: The Institute for Supply Management's index -- measuring the nation's non-manufacturing business activity -- rose to 53.2 in September, from 51.5 the previous month. Economists were expecting the gauge to inch up to 51.8. Any number above 50 indicates growth in the sector.

Currencies and commodities: The dollar fell sharply against major currencies Tuesdays, with the dollar index touching its lowest levels since January.

The greenback sank to an 8-month low against the euro, and also slipped versus the British pound and the Japanese yen.

"There's a very bearish tone toward the U.S. dollar regardless of the broader economic conditions around the globe," said Gareth Sylvester, senior currency strategist at HIFX in San Francisco. "The market is largely fixated on the story of a weak domestic economy and therefore a weak dollar."

The dollar has been under pressure since the Federal Reserve announced it may buy long-term U.S. Treasurys to boost the economy. While the Japanese central bank announced a similar move for its economy, it didn't help curb the strength of the yen.

Rather, the dollar fell to the lowest level against the yen since the Japanese government announced intervention, a 15-month low. News of fiscal woes in Ireland have been largely ignored as well, Sylvester said.

"The currency market has a blinkered attitude at the moment" he said. "But if upcoming economic data consistently shows that the worst of the U.S. economy has been seen, investors may start to shift focus."

The buck's softness has helped boost prices of commodities priced in U.S. dollars, including gold and oil.

Gold futures for December continued to run in record territory. Prices spiked $23.50 to settle at an all-time high of $1,340.30 an ounce, after reaching a fresh intraday record trading high of $1,342.60 an ounce earlier Tuesday.

The price of crude oil for November delivery rose $1.35 to settle at $82.82 per barrel.

Bonds: Prices for U.S. Treasurys rose, pushing the yield on the 10-year note down to 2.47% from 2.48% late Monday. Bond prices and yields move in opposite directions.

Stocks finish near session lows

NEW YORK (CNNMoney.com) -- Stocks finished near session lows Monday following a midday sell-off, with the Dow and Nasdaq indexes posting their largest one-day losses in nearly a month, as investors remain cautious ahead of corporate earnings season and key employment data due later in the week.

The Dow Jones industrial average (INDU) tumbled 78 points, or 0.7%, with components Intel (INTC, Fortune 500), Alcoa (AA, Fortune 500), American Express (AXP, Fortune 500) and Microsoft (MSFT, Fortune 500) sinking the most.

The S&P 500 (SPX) lost 9 points, or 0.8%. The Nasdaq (COMP) dropped 26 points, or 1.1%, with a Microsoft downgrade dragging the tech-heavy index lower. Other big tech shares losing ground included Apple (AAPL, Fortune 500) and Google (GOOG, Fortune 500).

Stocks started the day near the breakeven point, but selling accelerated as the session wore on. With little on the economic docket to attract investors, the September rally has lost its momentum.

"We're just seeing a pullback from that," said Peter Cardillo, chief market economist at Avalon Partners. "We're going to get the monthly jobs report later this week, so volume will be light and the market could be volatile ahead of that release."

A report showing a continued slowdown in manufacturing, coupled with data showing some pickup in the housing market, did little to stem the jitters on Monday.

"We'll continue to see a lot of mixed signals," said Karl Mills, president and chief investment officer at Jurika Mills and Keifer. "I think it will be hard for the market to repeat as strong of a month as what we just saw, but it'll depend on the companies' earnings and their outlooks."

Alcoa kicks off the unofficial start of earnings season after the closing bell on Thursday. Investors will also be gearing up for the government's monthly jobs report, due out Friday.

Stocks had started October on a positive note -- although Friday's advance was limited. But with economic uncertainty continuing to underpin the markets, investors could be in for a rough month.

Economy: A report from the Commerce Department showed that factory orders fell 0.5% in August, heightening fears about a slowdown in U.S. manufacturing growth. Economists were expecting order to decrease by 0.4%.

The National Association of Realtors said pending home sales rose 4.3% in August. Economists were expecting the report to show a mere 1% uptick in sales. But pending home sales only indicate contracts being signed and not actual closed purchases.

Companies: Shares of American Express tumbled 6.5%, after the Department of Justice filed an antitrust lawsuit against the company. The credit card giant said it has "no intention of settling the case."

The suit comes as rivals Visa (V, Fortune 500) and Mastercard (MA, Fortune 500) settled their antitrust case regarding their credit card policies. Neither company admitted any wrongdoing.

French pharmaceutical giant Sanofi-Aventis (SNY) launched a hostile takeover of Genzyme (GENZ, Fortune 500). Sanofi said it was taking its $18.5 billion offer for its rival directly to shareholders, after its efforts to work with the board of Genzyme were "blocked at every turn." Shares of Sanofi fell 0.8%, while Genzyme's stock rose 0.2%.

Shares of Sara Lee (SLE, Fortune 500) climbed 7.2%, after the New York Post reported that the company turned down a $12 billion buyout offer from investment firm KKR & Co.

Microsoft (MSFT, Fortune 500) fell 1.9%, after the tech giant's shares were cut by a Goldman Sachs analyst.

World markets: European stocks declined Monday. The CAC 40 in France and Germany's DAX closed down at 1.2%. Britain's FTSE 100 fell 0.7%

In Asia, the Hang Seng gained nearly 1.2%. Japan's Nikkei finished the session down 0.3%. The Bank of Japan started a two-day policy meeting. The Shanghai Composite was closed for Golden Week.

Currencies and commodities: The dollar rose against the euro and the Japanese yen, but fell slightly against the British pound.

Gold futures for December delivery fell $1 to settle at $1,316.80 an ounce.

The price of crude oil for November delivery fell 11 cents to settle at $81.47 per barrel.

Bonds: Prices for U.S. Treasurys rose, pushing the yield on the 10-year note down to 2.48% from 2.51% late Friday. Bond prices and yields move in opposite directions. The 2-year yield touched a record low just below 0.40%

Stocks post best September in 71 years

NEW YORK (CNNMoney.com) -- U.S. stocks fizzled Thursday, but that didn't stop the market from logging its best September in decades.

Dow Jones industrial average (INDU) slipped 47 points, or 0.4%, after soaring more than 100 points at the start of trading. The S&P 500 (SPX) fell 4 points, or 0.3%, and the Nasdaq (COMP) ticked down 8 points, or 0.3%.

Economic jitters have kept stocks from breaking out of a narrow range this week. And while upbeat readings on employment and economic growth helped spark an early rally Thursday, gains subsided as worries about the euro zone bubbled up.

Despite the stomach churning month, stocks ended September on a high note. The Dow jumped 7.7%, the biggest September gain in 71 years. The S&P also posted the biggest gain since 1939, rising 8.7% in the month, while the Nasdaq climbed 12%.

All 30 Dow components were on track to end September with gains, as of Wednesday's market close. Caterpillar (CAT, Fortune 500), Alcoa (A, Fortune 500), GE (GE, Fortune 500), Home Depot (HD, Fortune 500) and 3M (MMM, Fortune 500) are among the biggest gainers.

And only 18 of the S&P 500 were down on the month. Carmax (KMX, Fortune 500), JC Penney (JCP, Fortune 500) and Office Depot (ODP, Fortune 500) are among the biggest gainers on the broader index.

"There was a lot of talk this summer about a double-dip recession, and while it's true things have slowed down, the technicals have really changed and it's a much more healthy environment now," said Kenny Landgraf, principal at Kenjol Capital Markets.

Economy: The number of Americans filing for unemployment insurance edged down to 453,000 in the week ended Sept. 25, according to the Labor Department. The figure was slightly better than the 457,000 jobless claims economists had expected.

"The big bash against this recovery has been that it's a jobless recovery ... so investors are obviously going to take that [report] well," said Landgraf.

Meanwhile, the Commerce Department released its final reading on second-quarter gross domestic product, raising it slightly to a gain of 1.7% from the previously reported 1.6%.

Economists surveyed by Briefing.com had expected the figure to remain unchanged.

World markets: Despite the wave of upbeat readings on the U.S. economy, bad news from overseas reignited fears about a slowing global recovery.

Ireland's central bank unveiled a bank bailout that could reach about $46 billion. Ireland's budget deficit is on track to hit 10 times the European Union guidelines for eurozone members. Meanwhile, Moody's downgraded Spain's credit rating.

"These are just further signs that we've covered up the European financial situation and tried to push it aside, but it's really still a big issue," said Dean Barber, president of Barber Financial group.

European stocks slumped. France's CAC 40 fell 0.6%, Britain's FTSE 100 dipped 0.4% and Germany's DAX lost 0.3%.

Asian markets shares ended mixed. The strong yen continues to plague Japanese stocks, with the Nikkei ending down 2%. The Hang Seng in Hong Kong lost 0.1%, while the Shanghai Composite rose 1.7%.

Companies: AIG (AIG, Fortune 500) took a major step toward paying back its government bailout Thursday, after announcing an agreement to pay down its debt to U.S. taxpayers. Part of this includes the insurer's plan to sell its Japan-based units for $4.8 billion. Shares of AIG gained more than 4%.

Shares of Johnson & Johnson (JNJ, Fortune 500) slipped less than a percent after CEO William Weldon took responsibility for the company's recall issues and admitted to hiding a Motrin recall effort.

Overall, Johnson & Johnson's stock has emerged unscathed from the recall issue as investors have largely shrugged off the issue since there were no reports of people getting sick.

Currencies and commodities: The dollar rose against the euro and the British pound, but fell versus the Japanese yen.

On Wednesday, Congress overwhelmingly passed legislation to impose tariffs on China for undervaluing its currency, the yuan, in order to keep export prices cheap.

Gold futures for December delivery slipped 70 cents to settle at $1,309.60 an ounce, after hitting another intra-day trading record of $1,316.20 an ounce earlier in the session.

Crude oil futures for November delivery gained $2.11 to settle at $79.97 a barrel.

Bonds: The price on the benchmark 10-year bond fell, pushing up the yield up to 2.52% from 2.5% late Wednesday.

DOW JONES and S&P500 . . . . NO.

SSE, SZSE, STI and some other Asian countries indices . . . YES.

iPunter ( Date: 30-Sep-2010 07:03) Posted:

|

This is a non-event....

Market resilience, or stability is still intact..

Stocks stumble at the close

NEW YORK (CNNMoney.com) -- U.S. stocks ended slightly lower Wednesday, as uneasiness about the global economy continued to hang over the market and a light economic calendar gave investors little reason to jump in.

Dow Jones industrial average (INDU) slipped 23 points, or 0.2%, the S&P 500 (SPX) fell 3 points, or 0.3%, and the Nasdaq (COMP) lost 3 points, or 0.1%.

After rallying to 4-month highs and gaining for a fourth straight week last week, stocks have been stuck in a rut, swinging between small gains and losses.

"The economy still hasn't improved measurably," said Brian Battle, director of Performance Trust Capital Partners. "If there is a recovery taking place, it's very uneven."

Stocks finished modestly higher Tuesday, but trading was choppy as a disappointing reading on consumer morale fueled worries about the recovery.

While the economy may not be headed for a double-dip recession, economic and political uncertainty ahead of midterm elections and new tax policies is making it hard for stocks to keep up their momentum, said Tom Schrader, managing director at Stifel Nicolaus.

"Markets hate uncertainty, and the government has created a tremendous amount of uncertainty, so that's gotten the market frozen," he said. "It's not that we're going to get a double-dip recession, it's much more likely that we flatline for some time as small businesses and individuals are very cautious about what the government has done and what it's going to do."

World markets: With little in the way of economic news on tap Wednesday, concerns about the health of the euro zone pressured global markets.

European stocks slumped. Britain's FTSE 100 finished 0.2% lower, Germany's DAX declined 0.5% and France's CAC 40 dropped 0.7%.

Amid austerity measure protests in Spain, Ireland and Brussels, news reports Wednesday said Allied Irish Banks PLC may need an additional capital boost to protect it from future losses. Moody's downgraded Anglo Irish earlier this week.

"The weakness of European markets is all about concerns in Europe in terms of what the Irish are going to do with [Allied Irish Banks], we have strikes in Spain, and just the whole upheaval in the European continent," said Schrader.

Meanwhile, the U.S. House of Representatives was considering a bill that could punish China for manipulating the yuan's value, despite China's pledge Wednesday to increase the flexibility of its exchange rate.

"The U.S. Congress wanting to tick off our largest trading partner certainly doesn't bode well for the market," Schrader said.

Asian markets ended mostly higher. Japan's Nikkei added 0.7% and the Hang Seng in Hong Kong rallied 1.2%. The Shanghai Composite finished near breakeven.

Currencies and commodities: The dollar also suffered Wednesday, as worries about the recovery boosted speculation that the Federal Reserve will step in sooner rather than later to provide additional support to the U.S. economy.

The greenback fell against the euro and the Japanese yen, but rose versus the British pound. The U.S. Dollar Index -- which tracks the dollar against a basket of currencies -- fell 0.4% after sinking to its lowest level in eight months earlier in the day.

Gold for December delivery continued to break records Wednesday, gaining $2 to settle at an all-time high of $1,310.30 an ounce after hitting an intra-day trading record earlier in the session.

Crude oil futures for November delivery gained $1.68 to settle at $77.86 a barrel.

Bonds: The yield on the benchmark 10-year bond rose to 2.5% from 2.46% late Tuesday.

Companies: AIG is reportedly preparing to sell two of its Japanese life insurance divisions to Prudential Financial Inc. for $4.8 billion in cash, according to Bloomberg News. Shares of AIG edged slightly higher on Wednesday.

The U.S. government and AIG (AIG, Fortune 500) are also reportedly working out a deal that would allow the Treasury Department to gradually exit its majority stake in the insurer.

Shares of AOL (AOL) climbed 4.6% Wednesday after the media giant added another blog to its portfolio on Tuesday, buying technology blog TechCrunch.

Hulumas, what price was China Jishan at its lowest? Tks

Hulumas ( Date: 29-Sep-2010 10:14) Posted:

|

iPunter ( Date: 28-Sep-2010 20:54) Posted:

|

iPunter ( Date: 29-Sep-2010 07:57) Posted:

|

Stocks claw out gains

NEW YORK (CNNMoney.com) -- U.S. stocks finished higher Tuesday as a drop in consumer confidence and a mixed reading on home prices failed to sink recovery hopes.

The Dow Jones industrial average (INDU) climbed 46 points, or 0.4%, the S&P 500 (SPX) added 5.5 points, or 0.5%, and the Nasdaq (COMP) gained 10 points, or 0.4%.

After rallying for a fourth straight week last week, stocks slipped from 4-month highs and ended the day lower Monday amid a flurry of deal-making activity and ongoing economic jitters.

Despite a disappointing report on consumer morale early Tuesday that initially sent stocks tumbling, investors haven't given up hope that a recovery is gradually gaining pace, said Mark Luschini, chief investment strategist at Janney Montgomery Scott.

"The sentiment is that economic data has not necessarily improved significantly from summer months, rather it has stopped showing signs of deterioration," said Luschini. "But that's enough for some people to suggest that the risk of a double-dip recession is receding."

Economy: The Consumer Confidence Index dropped to 48.5 in September from a downwardly revised 53.2 in August, the Conference Board reported. Economists had been expecting the number to edge to 53. The index is a far cry from 90 -- a level that typically indicates a stable economy.

"This is further evidence that the consumer is still not feeling particularly upbeat about what they see going on in the market or in the foreseeable future, which obviously impacts their spending behavior," said Luschini. "That's enough to hold markets back."

But the disappointing reading on consumer morale was countered by a slightly encouraging report on home prices.

The Case-Shiller 20-city home price index showed home prices inched up 0.6% in July compared with June, according to the S&P/Case-Shiller 20-city home price index. On a year-over-year basis, prices rose 3.2% compared with July 2009. Experts polled by Briefing.com had forecast a year-over-year rise of 3.3%.

"It wasn't robust, but the [reading] represents more normalized traffic coming into the market, which is helping to put a floor into housing prices," said Luschini. "It's too soon to suggest a recovery in the housing market, but this at least suggests we're bringing some stability to this beleaguered but critical area of the economy."

Stuck in a rut?: While a double-dip recession may be becoming less of a concern, it's going to take more than a slew of lackluster economic readings to push the market significantly higher, said Ron Kiddoo, CIO at Cozad Asset Management.

"We've had a good move up this month and economic readings have been slowly getting better," he said. "But we still need to see much better economic numbers, and that just isn't happening."

With midterm elections around the corner and as investors await the government's closely-watched jobs report on tap next week, political and economic uncertainty is likely to keep stocks in a tight trading range.

"I don't expect [economic] numbers to get a lot better for a while, which could mean the remainder of the calendar year," said Kiddoo. "Attempts of government spending and bringing in jobs aren't working and businesses are spending a lot of cash and doing well but are afraid to invest because they don't know what the future is going to bring in terms of taxes and legislation."

Companies: AOL (AOL) shares gained nearly 3% after the media giant announced plans to acquire news outlet TechCrunch.

Shares of Barnes & Noble (BKS, Fortune 500) closed slightly higher after the bookseller said shareholders rejected investor Ronald Burkle's bid to expand his ownership of the company.

Meanwhile, BlackBerry maker Research in Motion (RIMM) on Monday unveiled the PlayBook, a new tablet computer to compete with Apple's (AAPL, Fortune 500) iPad.

Shares of RIM slipped 3% Tuesday, and the stock is down about 30% this year due to concerns that the company is falling behind Apple, as well as smartphone makers using Google's (GOOG, Fortune 500) Android operating system.

Shares of Walgreens (WAG, Fortune 500) surged more than 11% after the drugstore chain reported its fiscal fourth-quarter revenue rose 7.4% to a record $16.9 billion, driven by strong prescription drug sales. The company's quarterly earnings rose 7.8% to $470 million, or 49 cents per share.

World markets: European stocks ended mixed. Britain's FTSE 100 edged up 0.1%, France's CAC 40 lost 0.1%, and Germany's DAX was flat.

Early Tuesday, European markets tumbled after a Spanish newspaper pointed out that Moody's deadline for reviewing its investment grade AAA credit rating for Spain runs out this week. The country could be facing a downgrade due to its sovereign debt troubles.

Asian markets ended the session in negative territory. Japan's Nikkei and the Hang Seng in Hong Kong each lost more than 1%. The Shanghai Composite fell 0.6%.

Currencies and commodities: The dollar fell against the euro and the Japanese yen, but rose versus and British pound.

Gold futures for December delivery surged $9.70 to settle at a new record of $1,308.30 an ounce, after hitting an all-time intraday trading high of $1,311 earlier Tuesday.

The price of crude oil for November delivery fell 34 cents to settle at $76.18 per barrel.

Bonds: Prices for U.S. Treasurys rose, with the yield on the 10-year note falling to 2.47% from 2.53% late Monday. Bond prices and yields move in opposite directions.

Dow futures are green at the moment...

Hope the Dow rises moderately and maintain it's resilience...

A huge "Cheong Aaarrrhhh!!! type of rally is not healthy,

whereas a gradual climb amidst a wall of worry is best...

Yup...better world for all. (less dangerous) To each and each everyone, hope there's better tomorrow and they shall be. (Trade war?) will come to term with it. U win some, I win some. If not then.![]()

World senior leaders tend to think alike this 21st century and for their own prosperity and though threat or whatever threat there is...it will not end prosperity in or for next few decades.

unless we have man like Adolf Hitler and or General Tomoyuki Yamashita from 20th century.

Hulumas ( Date: 28-Sep-2010 19:10) Posted:

|