Now HSI(-785) n STI(-76) suddenly down turn sharply. Suspect EU markets are down now. Teletext not updated yet.

All these expert analysis are questionable. Aren't they the one who advocate to buy in the first place? Their calls should always view with care.

haha u chose a easy path...

mikewb21 ( Date: 15-Oct-2008 15:41) Posted:

| Citi TP $1.5, CS TP $0.55,I think 1 over estimate and 1 under estimate, so take the middle path, TP should be $1, my 5c thots, vested at $0.8 |

|

Citi TP $1.5, CS TP $0.55,I think 1 over estimate and 1 under estimate, so take the middle path, TP should be $1, my 5c thots, vested at $0.8

14 October 2008 9 pages

Cosco Corporation (Singapore) (COSC.SI)

Downgrade to Hold: Rig Building Plans Put on Hold

v Customer financing challenges Our earlier thesis of Cosco capturing higher

value add rig business did not materialise. Customer Sevan Marine appears to

be having financing difficulties despite having secured charter contracts from

Petrobras. This has impacted Cosco's foray into the rig building segment.

v Revise Earnings Estimates We have i) lowered our FY08E-10E new order

assumptions to S$1.6-1.8bn from S$3.5-4bn; ii) reduced FY08E-10E gross

margin sharply; iii) lowered our assumptions for bulk carrier charter rates by

16-53% on weaker BDI. Our FY08E-10E estimates are reduced by 17-43%.

v New TP S$1.50 based on SOTP Valuation Our target price is based on i)

S$0.99/share for Ship Repair, Offshore & Marine business, based on ~6.5x

FY09E PER for the shipyard business (from 14.5x previously) to reflect its lack

of progress penetrating the rig building business a 70% discount over our

valuation for Singapore O&M peers; ii) S$0.20/share for the Shipping business

in line with yard valuations, iii) net cash of S$0.31/share.

v Downgrade to Hold; Raise Risk Rating to High We downgrade to Hold

from Buy as valuations appear to have priced in downside risks while positive

catalysts have yet to emerge. We increase the risk rating from Low to High Risk

for Cosco Corp, in line with our quantitative risk rating system.

v Please see our sector report: "Industry Risks Heightened Amid Credit Crunch"

dated 14 Oct 2008 for more details.

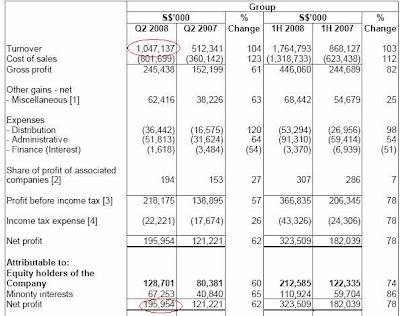

Figure 1. Cosco Corp Statistical Abtract

Which analyst ? May be there want to sale their cosco share. "MAY BE "

ekekeg ( Date: 15-Oct-2008 14:58) Posted:

Why there are another analyst report to hold and fair price $1.50 per share?

I already shorted so many lots, then the report comes in, say to hold. How now? |

|

Is it justified, guys?

We noted the beating of Cosco today. As of now 12.30pm ...trading between a range 0.94 - 0.76.Wow. We noted that DMG gave a sell call of this counter...stating some reasons and more reasons and much more reasons..qualitatively..which is true actually. We noted also BT had a report on it with Credit Suisse saying something about drifting lower.

But, let's take a step back..clear our heads a bit, relax..and think simply, shall we? Let's look at some quantitative figures....

Net Profit Margin:

Net Profit Margin: 18.71 % ( Ok still some room to maneurvure if demand sucks or supply sucks, compare again with

Ferrochina.!)

Debt repayment ability (sorry we refuse to use jargon, bear with us ok!):

Debt repayment ability (sorry we refuse to use jargon, bear with us ok!): CA less than CL. ( Hmm but its not that much of a shortfall. not like Ferrochina!)

Cash Flow Muscle:

Cash Flow Muscle: Pretty strong. As you see its Cash from Operations has been positive since 2003 and guess what..even after netting off capital expenditure ( the expenditure needed to sustain this business..in simplified terms) its still positive! ( Some people call it free cash flow..a jargon we prefer not to use) . This is a good sign!

SGDividends: Why are we wasting our time on this report? Cos here are SGDiviedends, we refuse to take Analysts reports seriously, Credit Suiise, DMG..blah blah blah... Look at the company's numbers first(MOST IMPT)..take care of its downside first..before using reasons like order book, economy slowdown,risk of order cancellation, delivery delays( which are of cos darn impt too) but kinda fluffy dont you think.

Our recommendation: Your Guess is as good as mine? Decide for yourself!

HANG SENG

HANG SENG NIKKEI 225

NIKKEI 225 Debt repayment ability (sorry we refuse to use jargon, bear with us ok!): CA less than CL. ( Hmm but its not that much of a shortfall. not like Ferrochina!)

Debt repayment ability (sorry we refuse to use jargon, bear with us ok!): CA less than CL. ( Hmm but its not that much of a shortfall. not like Ferrochina!) Cash Flow Muscle: Pretty strong. As you see its Cash from Operations has been positive since 2003 and guess what..even after netting off capital expenditure ( the expenditure needed to sustain this business..in simplified terms) its still positive! ( Some people call it free cash flow..a jargon we prefer not to use) . This is a good sign!

Cash Flow Muscle: Pretty strong. As you see its Cash from Operations has been positive since 2003 and guess what..even after netting off capital expenditure ( the expenditure needed to sustain this business..in simplified terms) its still positive! ( Some people call it free cash flow..a jargon we prefer not to use) . This is a good sign!